Manufacturing Overhead Is Best Described as:

C costs that are not economically feasible to trace directly to specific jobs or processes. All manufacturing costs other than direct materials and direct labor.

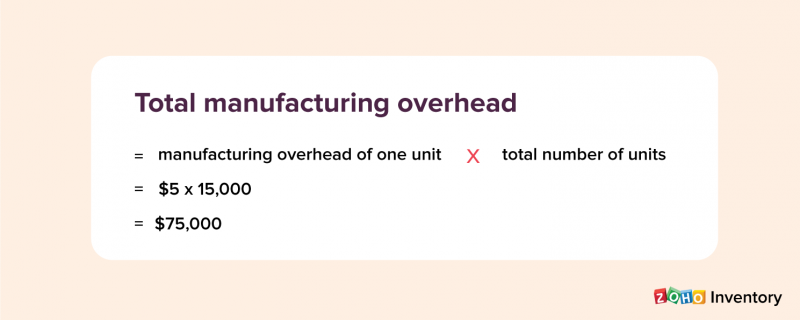

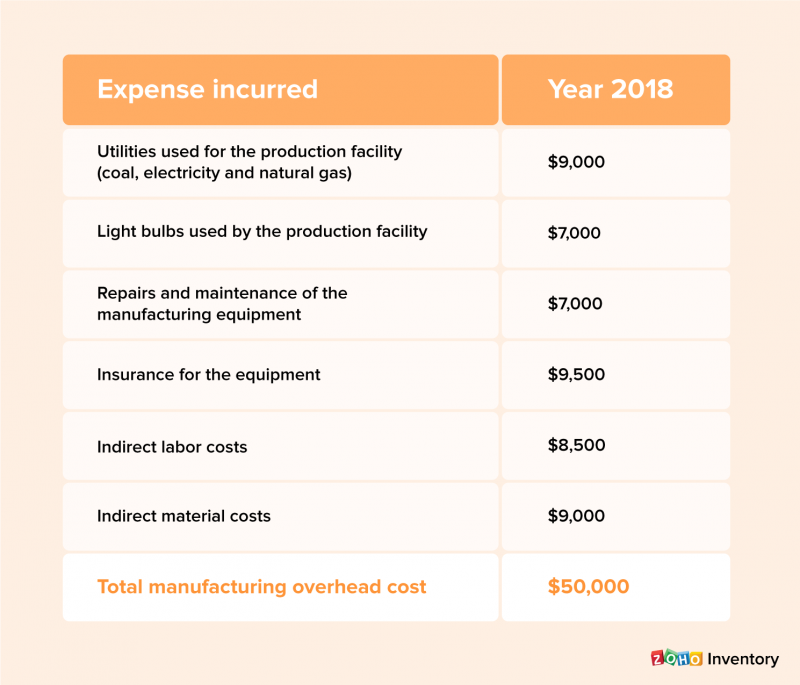

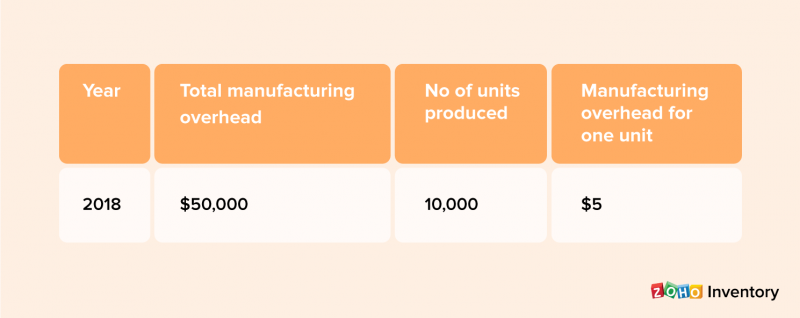

Manufacturing Overhead Moh Cost How To Calculate Moh Cost

Manufacturing costs are also known as product costs.

. Manufacturing overhead is best described as. Direct product costs d. Administrative conversion manufacturing overhead Manufacturing overhead is which type of cost.

B All period costs associated with manufacturing operations. Indirect period costs c. Direct period costs b.

Direct materials and direct labor only. Manufacturing costs incurred to produce units of output. All period costs associated with manufacturing operations.

All operating expenses other than selling expenses and general and administrative expenses. All manufacturing costs other than direct materials and direct labor. D costs that management has decided not to trace directly to specific jobs or.

The over or under-applied manufacturing overhead is defined as the difference between manufacturing overhead cost applied to work in process and manufacturing overhead cost actually incurred by the entity during the period. Direct material and direct labor costs are traced directly to the products as they flow through each production department. If the manufacturing overhead cost applied to work in process is more than the manufacturing overhead cost actually incurred during a.

A All manufacturing costs other than direct materials and direct labor. An imputed a relevant a variable The head of the accounting department in a very large manufacturing firm usually has the. Using absorption costing fixed manufacturing overhead costs are best described as indirect product cost.

A Direct materials direct labor and factory overhead. In the year-end financial statements the. It is indirect because it is not directly traceable to a specific unit and a product cost because it allocated to the product.

Manufacturing overhead is best described as. Manufacturing overhead is assigned in each department using separate departmental manufacturing overhead rates. Multiple Choice All manufacturing costs other than direct materials and direct labor.

Property taxes and insurance premiums paid on a factory building are examples of manufacturing overhead. Under absorption costing fixed manufacturing overhead is allocated to the units produced and it is best classified as an indirect product cost. Administrative expense direct product indirect product A cost that exists but is not explicitly stated is best described as cost.

Income under absorption costing may differ from income under variable costing. Are the differences in costs between any two alternative coursesnof action. Using absorption costing fixed manufacturing overhead costs are best described as _____.

Are anticipated future costs that will differ among various alternatives c. The sum of direct labor costs and all factory overhead costs. The sum of raw materials costs and direct labor costs.

All costs associated with manufacturing other than direct labor costs and raw material costs. Direct period costs c. Manufacturing overhead also known as factory overhead factory burden production overhead involves a companys manufacturing operations.

Under variable costing all product costs are variable. Which of the following best describes those costs which are considered to be manufacturing costs. It includes the costs incurred in the manufacturing facilities other than the costs of direct materials and direct labor.

Direct materials direct labor factory overhead and administrative overhead. A costs that cannot be traced directly to specific jobs or processes. Which of the following best describes those costs which are considered to be manufacturing costs.

Manufacturing overhead is best described as. B costs that are economically feasible to trace directly to specific jobs or processes. Are variable costs B.

Are costs that differs under alternatives. Using absorption costing method fixed manufacturing overhead costs are best described as indirect product cost. Hence manufacturing overhead is referred to as an indirect cost.

The difference in income between the two costing methods is equal to the change in the quantity of all units a. If the ending inventory of finished goods is understated net income will be overstated. Indirect period costs d.

Using absorption costing fixed manufacturing overhead costs are best described as. Manufacturing overhead combined with direct materials is known as conversion cost. Manufacturing overhead is best described as Multiple Choice All manufacturing from ACCT 420 at Metropolitan Community College Omaha.

Total Manufacturing costs are also known as product costs. Using absorption costing fixed manufacturing overhead costs are best described as. Direct product costs b.

Indirect materials and indirect labor. Direct materials direct labor and factory overhead. All operating expenses other than selling expenses and general and administrative expenses.

Under variable costing all variable costs are treated as product costs. In a manufacturing company goods available for sale equals the. Using absorption costing manufacturing overhead costs are best described as A.

Manufacturing overhead is best described as. All period costs associated with manufacturing operations. Indirect materials and indirect labor.

Manufacturing overhead is best described as. The inventory costing method that the manufacturing company is using in this situation is A. Under variable costing fixed manufacturing overhead costs are best described as a.

Manufacturing Overhead Double Entry Bookkeeping

Manufacturing Overhead Moh Cost How To Calculate Moh Cost

Manufacturing Overhead Moh Cost How To Calculate Moh Cost

Comments

Post a Comment